Return to Uzone News Portal

Return to Uzone News Portal

Uzone.id — Starting a tech company might look exciting, but little did you know it has tons of risks. Business is just a business, no company achieves success without facing challenges along the way. The key is learning how to navigate these obstacles and grow stronger through them.

When you start your startup, it means that you’re ready to face the risk ahead of you, from investors, legal battles with competitors to cash flow crisis.

To help you navigate these challenges, here are the most common risks that tech startups face and how you can protect and manage your business.

Lack of a Solid Business Plan

Running a startup without a clear business plan is like a road trip without a map and at the end, you’ll get lost. Poorly thought-out plans are a common reason for startups’ struggle. Having a business plan gives you clarity on where your company is headed.

According to Small Business Administration (SBA) data, startups that plan properly are 16 percent more likely to achieve viability than those that don’t.

Planning your business plan can start from the basics like executive summary, your product offerings, market analysis (including a SWOT analysis), financial projections, and funding goals are must-haves.

Do not forget to make a plan about your business growth, you can start by outlining your marketing strategy, business model, and team structure. This helps you avoid the temptation of rushing to market with a full-prep product.

Misjudging Market Demand and Competition

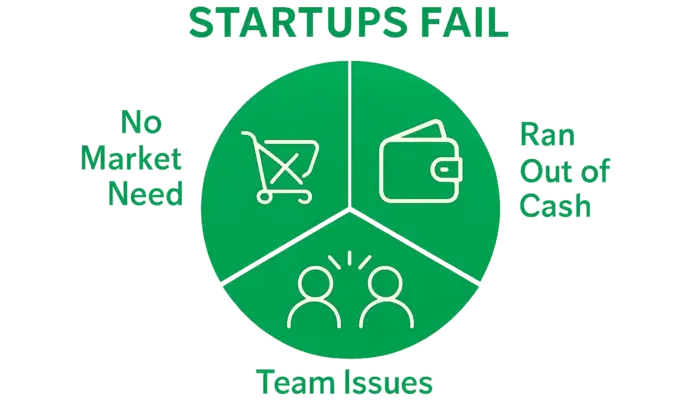

Misunderstanding your market and underestimating your competitors are common traps. Startups often think they’ve filled a market gap, only to find out there’s little demand for their product. According to CB Insights, 35 percent of startups fail because there’s no market need.

Market research is the main key to solve this problem. Spend time gathering data on customer preferences and competitor activity. Use free tools like Google Trends to gauge what’s hot and analyze reports from reputable organizations in your industry.

Don’t forget that we’re also living in the online world, using social media is also powerful to engage directly with your target audience. You can send surveys or run polls to find out what they truly need.

Keep an eye on your competitors. Tools like SEMrush or SimilarWeb allow you to track their marketing and product updates, giving you a competitive edge.

Low and Poor Quality Products

Many startups rush to launch without fully understanding who their target customers are or why those customers would buy their product. If your product is still in the development stage, don’t rush it.

Poor quality products can harm your reputation and may even result in lawsuits. If you offer a service as your output, consider Professional Indemnity Insurance, which can protect you against claims of negligence or mistakes.

To tackle this risk, start with a Minimum Viable Product (MVP) at the beginning of your production. You can test your product with customers and gather feedback without spending too much time or money.

“Get out and talk to customers. Your product might look great in theory, but it’s the customers who determine its success,” said Steve Blank, a leading figure in the startup ecosystem.

Cash Flow Problems.

One of the most common reasons for startups to fail is running out of cash. Even with a great product, mismanaging your finances can leave you scrambling. Data from CB Insights reveals that 29 percent of startups collapse due to cash flow issues.

So, start creating a financial plan that includes a budget that covers your operational expenses, projected revenue, and any debts or loans you’ve taken on. It’s digital era, using accounting software like QuickBooks or Xero can help you track your spending and adjust as needed.

Have a runway plan. Make sure you have enough funding to cover at least six months of operating expenses, especially if you’re pre-revenue.

Cybersecurity threats is not priority

With the rise of digital service and tech innovations these days, tech startups are prime targets for cyber attacks.

A report from Accenture showed that 43 percent of cyberattacks target small businesses, and only 14 percent are prepared. Another report by Kaspersky stated that around 13 million cyber threats attack companies in Southeast Asia.

That’s why companies should invest in Cyber Liability Insurance. This insurance covers the costs of data breaches, ransomware attacks, or lawsuits from clients who were affected by a breach. For a company, protecting sensitive data by encrypting files and communication is a must too. Make sure to use multi-factor authentication for your software and accounts.

Tech startups are full of potential but also come with their fair share of risks. Take the time to do your homework, plan properly, and invest in insurance to safeguard your business.

Keep these strategies in mind, and you’ll be in a much stronger position to protect your startup from hidden threats.